In my previous blog posted earlier this year we looked at the misconception regarding the liquidity of structured products. For this blog we are going to look at a subject which many advisers say is a reason they are not comfortable recommending structured products to their clients – COMPLEXITY.

So let us first look at what a Structured Product is:-

In other words, a structured product is simply an ‘IOU’ from a bank to a client. An agreement to pay a fixed amount on a set date if a certain condition is met. As an example, for a capital protected product, the provider will create (hedge) a product by combining:-

At maturity:

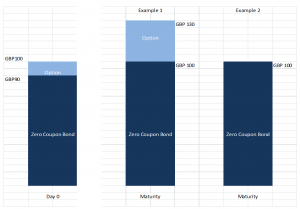

Let us assume that we launch a product that is structured as such:-

Example -1: the same or higher than the starting level the client will receive back 30%, plus their initial investment

Example- 2: lower than the starting level the client will just receive back their initial investment, however the initial capital is fully protected

As we can see from the above, at maturity the Zero Coupon Bond has grown from 90 to 100 which is the return of the client’s initial investment.

In example 1- the FTSE100 finished higher than its starting level and therefore the client has received a total return of 130%.

In example 2- the FTSE100 finished lower than its starting level, therefore the total return to the client is 100%

In this example product, the client has invested into a product, which in its simplest form is an IOU to the bank (this is where counterparty risk comes into play). Their return is either their initial investment back or a 30% gain. Whilst the bank may use options to hedge their risk, the client is not buying nor ever owns any options.

Of course, this is a very basic product and there are structured products which are more complicated but I think that in comparison to alternative investments, structured products should not be seen to be more complex. It is always important that the adviser and the client fully understand the risks involved in any investment, and here at Mariana we are happy to offer support and training to advisers who wish to understand or refresh their knowledge on this valuable investment tool.

Not found your answer? Live chat is the quickest way to get in touch with a real person at Mariana or call us on 020 7065 6699

Start live chat »